2025 Digital Media Trends: Social platforms are becoming a dominant force in media and entertainment

While studios and streaming providers are busy competing with each other, tougher competition is coming from social video platforms that are hyperscale and hyper-capitalized

China Widener

Jana Arbanas

Doug Van Dyke

Chris Arkenberg

Bree Matheson

Brooke Auxier

People still want the TV and movie experience offered by traditional studios, but social platforms are becoming competitive for their entertainment time—and even more competitive for the business models that studios have relied on. Social video platforms offer a seemingly endless variety of free content, algorithmically optimized for engagement and advertising. They wield advanced ad tech and AI to match advertisers with global audiences, now drawing over half of US ad spending.1 As the largest among them move into the living room, will they be held to higher standards of quality?

At the same time, the streaming on-demand video (SVOD) revolution has fragmented pay TV audiences, imposed higher costs on studios now operating direct-to-consumer services, and delivered thinner margins for their efforts. It can be a tougher business, yet the premium video experience offered by streamers often sets the bar for quality storytelling, acting, and world-building. How can studios control costs, attract advertisers, and compete for attention? Are there stronger points of collaboration that can benefit both streamers looking to reach global audiences and social platforms that lack high-quality franchises?

This year’s Digital Media Trends lends data to the argument that video entertainment has been disrupted by social platforms, creators, user-generated content (UGC), and advanced modeling for content recommendations and advertising. Such platforms may be establishing the new center of gravity for media and entertainment, drawing more of the time people spend on entertainment and the money that brands spend to reach them.

Our survey of US consumers reveals that media and entertainment companies—including advertisers—are competing for an average of six hours of daily media and entertainment time per person (figure 1). And this number doesn’t seem to be growing.2 Not only is it unlikely that any one form of media will command all six hours, but each user likely has a different mix of SVOD, UGC, social, gaming, music, podcasts, and potentially other forms of digital media that make up these entertainment hours.

We want to hear

from you!

Complete a brief survey to provide your views on thought leadership content.

{kind=link}

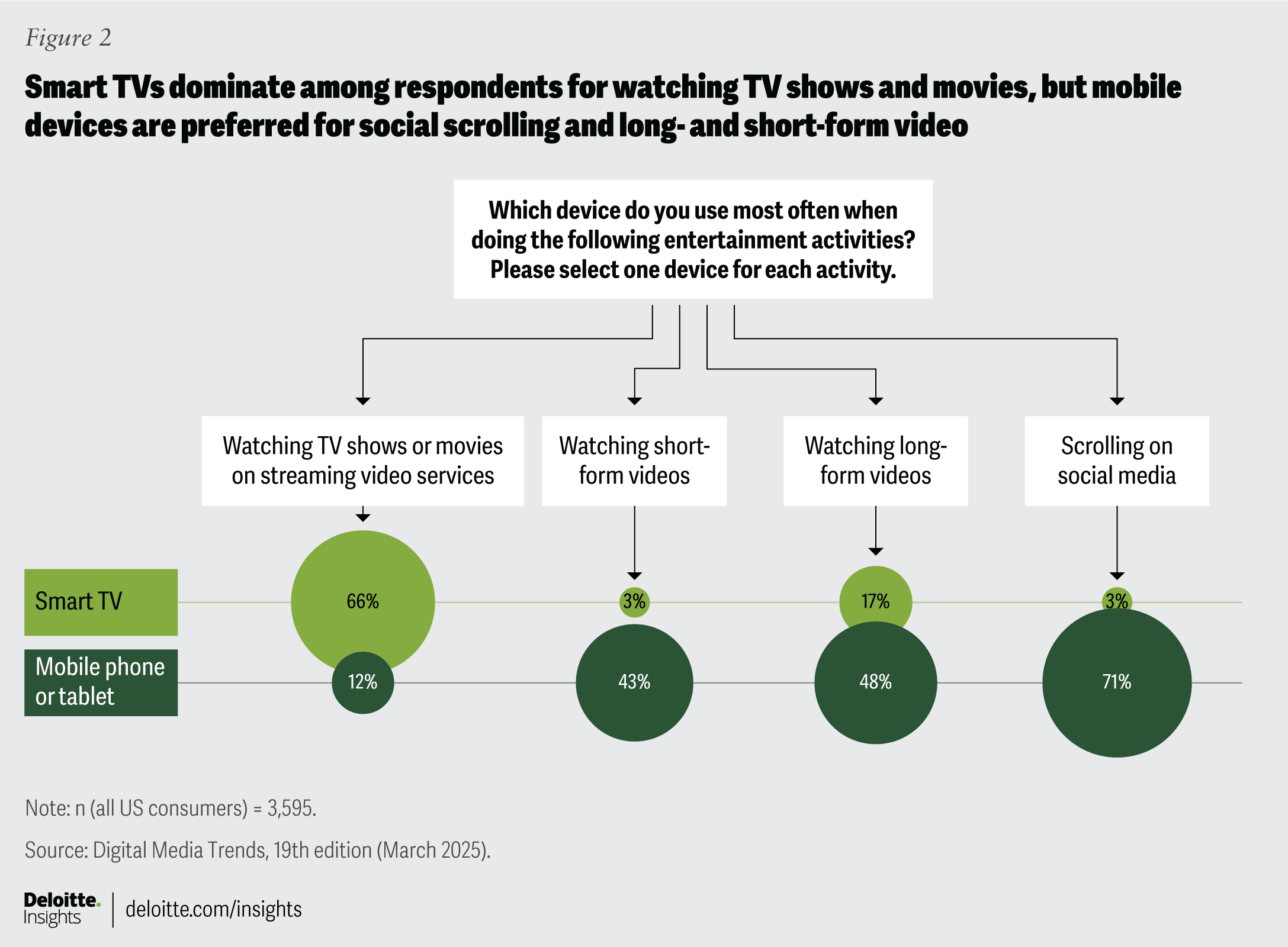

Looking across generations, preferences among respondents appear to be shifting away from pay TV and toward streaming video services, social video platforms, and gaming. Although TV once dominated video entertainment time, we now see US audiences—and especially younger generations—engaging more evenly with SVOD companies, social platforms, gaming, and even audio entertainment like music and podcasts. And they are using different devices to consume media (figure 2).

{kind=link}

This can further fragment the landscape of entertainment and make it more challenging for services and brands to reach audiences, and for providers to gather more people onto their services. With growing production and marketing costs, traditional studios and streamers are responding with more bundles and aggregations seeking to bring together disparate audiences, offer them lower prices for multiple services, and sell access to advertisers.3

Media and entertainment companies may also be competing for a fixed amount of entertainment spending. We do not see those surveyed spending more money on subscriptions, and many report fatigue with having to manage multiple subscriptions to get the content they want, and frustrations with rising subscription prices. The median household annual income in the United States is about US$80,000 and is only now rebounding from COVID-19 pandemic declines that began in 2020.4 At the same time, consumer prices have climbed for most goods.5 In Deloitte’s January 2025 ConsumerSignals survey, about half of US households say they have no money left over at the end of the month after meeting their expenses.6 This can shift the household calculus to prioritize spending on essentials over discretionary entertainment. Twenty years ago, many households may have considered pay TV an essential cost. Since then, the number of digital entertainment options has grown significantly, but the amount of time and money available for it have not. This has enabled greater consumer choice, more competition, and more fragmentation.

Pay TV: Making money but losing audiences

Cable and satellite television7 remain significant players in media and entertainment, though subscriptions continue to decline. We found that 49% of consumers surveyed currently have a cable or satellite TV subscription, down from 63% three years ago.8 The primary reasons subscribers report paying for these services are to watch live news (43%) and sports (41%). However, the market continues to fall, likely because SVOD services now offer more live sports options, and social media provides free sports clips and news recaps.

Older generations are more likely to maintain cable or satellite TV subscriptions, but 23% of Generation Z and 18% of millennial cable subscribers intend to terminate their subscriptions within the next 12 months, compared to only 8% of boomers.

Cost is likely a factor for these younger subscribers looking to cancel: Subscribers report spending an average of $125 per month on their cable or satellite TV subscriptions, which is significantly higher than the $69 on average subscribers report spending for four paid streaming services combined, according to our Digital Media Trends data. Subscribers also feel frustration with the number, and quality, of ads they’re required to watch at this higher price point.9

Live-streaming TV services offer an alternative, are slightly more popular with younger generations surveyed, and live-streaming TV subscribers in our survey report spending 35% less monthly on average for these services than cable or satellite subscriptions, but their growth has stagnated at around 40% of households for the past two years.10 A likely challenge is that these services tend to cost more than ad-free SVOD services, with pricing that seems to target existing pay TV subscribers accustomed to such costs, rather than younger generations gravitating to much cheaper— or free—media alternatives.11

Although cable and satellite subscriptions are falling, and live-streaming TV subscriptions appear stagnant, some in younger generations still show interest in live programming: Forty-three percent of Gen Z and millennials surveyed indicate a willingness to pay more for streaming video subscriptions that include access to live sports, although their engagement with live content remains to be seen. When asked about the types of content they spend the most time watching on SVOD, 27% of consumers said live sports, and just 8% said live events like music concerts. This may be due to a lack of options for those categories on SVOD, along with the ability to watch this content in other places: a third of Gen Z respondents say they don’t subscribe to an SVOD service to watch sports because they watch the clips and highlights on social media.

One challenge is that traditional studios still draw considerable revenues from their pay TV businesses.12 As they bring advertising to their streaming services, they may be hoping to migrate those pay TV ad revenues along with their audiences. However, global ad revenues for TV, including streaming video, are expected to see slow growth of around 2.4% in coming years, significantly less than overall advertising.13

Streaming video services: balancing value and frustrations

A similar tension seems to exist with streaming video services, which have subscription costs that may outweigh their perceived value. Fifty-three percent of consumers surveyed say their SVOD subscriptions are the paid media and entertainment services they use most frequently. However, 41% percent of consumers overall say the content available on SVOD isn’t worth the price, up five percentage points from our 2024 report.14 At the same time, roughly half (47%) of consumers say they pay too much for the streaming services they use, suggesting there is an imbalance between cost and perceived value. Indeed, while the average number of paid SVOD services has remained the same, at four per subscribing household, the overall cost subscribers surveyed say they pay has gone up 13% in the past year, from an average of $61 per month to $69. Gen Z and millennials, with an average of 5 paid SVOD services, have seen a 20% increase (figure 3).

{kind=link}

Currently, the average price for a premium, ad-free SVOD service subscription is around $16 per month, though the leading services can be significantly higher.15 However, according to Digital Media Trends data, consumers surveyed say that $14 is “just the right price” to pay for an ad-free subscription to their favorite SVOD service, with $25 being deemed too expensive (figure 4).

{kind=link}

Keeping in mind that not all SVOD services on the market have the same pricing power,16 the current average SVOD price is inching toward a critical price threshold, beyond which subscribers may be unwilling to pay. Respondents say that a price hike of $5 would make the majority (60%) of them likely to cancel their favorite SVOD service. Even their favorite services may be getting too expensive for the value, though it seems that so far, a few leading services have been able to raise prices significantly without losing subscribers. This can put more pressure on smaller services with less pricing power.

These rising service costs and widespread price sensitivities may be contributing to persistent—and high—SVOD churn rates among consumers. According to the survey, 39% of consumers say they have cancelled at least one paid SVOD service in the last six months (the measurement for churn)—a number that has remained relatively stable for the past several years.17 However, these churn numbers jump to above 50% for both Gen Zs and millennials who are also more likely to be strong social media users and gamers. Churn and return—or the percentage of consumers who have cancelled a service only to renew that same service in the past six months—also remains stable at 24%.

Service cancellations are problematic for streaming video on-demand companies that have been dependent on subscription revenues to support their costs, especially given the costs of acquiring—and possibly re-acquiring—subscribers. Some are bundling with other service providers to add value and lower subscriber costs, including creative bundles that tie SVOD services to less discretionary household spending.18 Many of the top streaming video providers are also launching ad-supported subscriptions, shifting their businesses more towards advertisers looking to reach large audiences. However, this may be leading them into more challenging territory.

Can studios compete for ad dollars?

Studios are not only competing for attention time—those six hours per day—and for subscription fees, but they’re also increasingly competing for advertising dollars. To curb outright cancellations, cast a wider net of subscribers, and generate revenues, some major SVOD services have introduced ad-supported tiers. These tiers offer cheaper subscription prices, but in exchange, users must watch advertisements. More than half of SVOD subscribers (54%) surveyed say that at least one of the services they pay for is ad-supported, a number that’s increased by eight percentage points since our 2024 report (figure 5).19 The average monthly cost for the ad-supported tiers currently on the market sits at around US$9,20 which is on par with the price respondents say is just right to pay (US$10) in exchange for watching eight minutes of ads per hour.

{kind=link}

Additionally, we found that more than two-thirds of younger generations subscribe to a free ad-supported TV service—streaming video services that are free to watch and fully subsidized by advertising. We also found that most respondents believe there is too much repetition of ads on streaming video services and cable.

Studios may hope they can migrate pay TV ad dollars to their streaming services, and that cheaper ad-supported tiers will make it easier to acquire and retain subscribers. However, the advertising landscape—and ad tech especially—is more mature outside of pay TV, and most digital ad dollars are now going to social platforms.21

Once again, the technological advantage that social platforms have built becomes apparent. Gen Zs (63%), followed by millennials (49%), are much more likely to say that ads or product reviews on social media are most influential to their purchasing decisions. Ads on streaming video services are a distant second (28% and 25%, respectively) (figure 6). Additionally, 54% of these younger generations surveyed say that social media ads are more relevant to them than those on streaming video services or cable TV.

{kind=link}

Leading social platforms are optimized for advertising, leveraging the same engines they use to deliver more relevant content to users, buoyed by accelerating spending on artificial intelligence. We found that a majority of Gen Zs and millennials surveyed say they get better recommendations for TV shows and movies from social media than from streaming video services. Social platforms can also make it easy for advertisers to buy ads and target specific cohorts with clear results.22 While traditional studios have spent heavily on streaming distribution and premium content, social platforms have been investing in data-driven personalization for both content creators and advertisers.23

The changing faces of video entertainment

Given these trends, it may be unsurprising that 56% of Gen Zs and 43% of millennials surveyed report that social media content is more relevant to them than traditional content like TV shows and movies (figure 7). Gen Zs lead the trend: These respondents spend 54% more time—or about 50 minutes more—than the average consumer per day on social platforms and watching UGC; and 26% less time—or about 44 minutes less per day—than the average person watching TV and movies.

{kind=link}

A draw toward social video platforms is the creators themselves. A majority of those in the younger generations we surveyed say creators’ videos are their favorite types of videos on social media. But perhaps more salient: Roughly 50% of Gen Zs and millennials surveyed say they feel a stronger personal connection to social media creators than they do with TV personalities or actors. Fans of creators often form parasocial relationships, which ups their investment and keeps them scrolling.24 For younger generations especially, trending social videos are often like the new hit TV shows and creators are the new reality stars..

This highlights another competitive twist. Top studios are spending more than ever to produce content for their services.25 Yet video content is increasingly being produced by independent creators and consumed on social platforms. Creators work for themselves, the platforms have options of how to incentivize them, and audiences get the content for free from algorithms designed for attention and engagement. Social platforms are extending generative AI tools to help creators run their businesses, create content, target audiences and advertisers, and match with brand sponsors.26 Creators offer more credibility and authenticity to brands and advertisers who may be trying to reach the millions who follow an influencer or the thousands who follow a trusted niche creator.27

Despite (and sometimes because of) their success, some creators have made the leap to network television or major streaming video platforms—where they can secure lucrative and stable contracts, get more exposure, and grow their audiences. This approach is met with mixed reviews: Some consumers surveyed say they’d be more willing to watch TV shows or movies starring their favorite creators (29% of consumers overall), while others say that creators lose the authenticity they had on social media when they’re featured on TV shows (30% of consumers overall) (figure 8).

{kind=link}

It’s worth noting, too, that this cross-medium success can work in both directions. That is, consumers surveyed say they often follow reality stars or athletes on social media after seeing them on a reality show or playing in a game—a behavior that is common for around 40% of both Gen Zs and millennials. In the same way that creators are amplifying their fame in TV and movies, more traditional celebrities are establishing themselves as brands, and amassing followings, on social media.

These last points suggest a deeper cultural shift: The definition and value of “celebrity” seem to be changing. Younger generations are spending more time on social platforms engaging with independent content creators who may seem more familiar and authentic, and spending less time with traditional celebrities who may seem distant, mainstream, and inauthentic.

Some studios may need to get bigger to survive

The costs of producing and distributing TV and films continue to go up, while the revenue they generate has gone down.28 The majority of advertising now goes to social platforms and hyperscale competitors—a handful of global, trillion-dollar companies with multiple lines of business and the most advanced AI capabilities available.29 Meanwhile, more studios are separating their pay TV businesses for potential divestiture, and focusing on their “core” business: intellectual property (IP) and streaming.30 Yet, the content and ad engines on most streaming video services are not yet mature, nor do they have the scale of data and expertise that has been acquired by social platforms. Accordingly, more studios are now working to advance their ad tech capabilities.31 And, some studios are beginning to distribute their programming on top of social video platforms. This could benefit both parties.32 Studios can learn from social platforms about content creativity and advertising capabilities, while platforms can benefit from the premium storytelling that is the strength of studios.

Yet, they’re all vying for a share of those six hours of daily entertainment time. This sharpens the new competitive landscape: Traditional studios face new competitors that are much larger than nearly all traditional TV and film studios combined.33 Leading social video platforms measure their global audiences and the hours of video viewed each day in the billions.34 And they dominate global advertising.35 If studios haven’t yet embraced this new reality, they face an imperative to change: Engagement with these platforms is eroding time spent on streaming TV and movies.36

Some traditional studios have been squeezing everything they can from their pay TV ad revenues, carefully migrating IP to their streaming services, spending on content to compete with other studios, and trying to get audiences and advertisers to make the journey with them. Bundles, especially with more essential and fixed services, and reaggregation of audiences to sell to advertisers might help.37 Some are building ad platforms that combine multiple streamers into one addressable ad market, hoping to make it easier and more cost-effective for advertisers to reach their audiences.38

Good TV can be touching and engrossing. Good cinema can be deeply impactful and moving. There is still value and demand for premium video content, but the economics likely need to be reset. Production costs are high and production times long. Fewer shows and films get produced and far fewer become big enough to cover their costs.39 This can make creativity risky: The safety of known successes is often preferred.

At the same time, many households are under financial pressure. Adding another paid subscription is not trivial. It likely either needs to deliver real ongoing value to justify the cost or the cost needs to come down. The former path requires more spending on content, and the latter more spending on advertising solutions. At a time when studios are looking to cut costs, facing the competition with social video is likely going to require significantly more spending.

Studios should consider the following.

- Advertising technology and AI are moving to the center of content economics. Studios should invest in ad tech to deliver more affordable and effective impressions and conversions. Strategic partnerships may be better needed to unlock these capabilities.

- Studios should gather larger audiences, potentially through mergers and acquisitions or clever aggregation, finding world-class ad tech partners to help them compete in the new ad landscape.

- Adopt technology quickly. Look to virtual production and AI to enable cheaper and faster production; generative AI for dubbing and translation to cross language barriers; and software and AI capabilities that can automate more operational functions, like contracts, script evaluation, and finding film locations. Much of this may require modernizing operations and finance.

- Social platforms are the nexus of discovery, awareness, and hype for film and TV: Fifty-six percent of younger generations surveyed watch TV shows or movies on SVOD after hearing about them from creators online, and 53% say they get better recommendations on what to watch from social media. Marketing efforts should start and end on leading social platforms.

- The fear that short form doesn’t work for premium IP may be mislaid.40 Get creative and publish to social platforms. Social video can help lift TV and movies.41

- Social content creators can be the strongest advocates—or opponents—of studio creativity, talent, and storytelling. They can help you engage audiences and communicate with them with greater authenticity. And they may be keys to unlocking virality and shaping culture.42

It may be that only hyperscale and diversified media companies can compete in the new landscape. Strong studio streamers—only a handful—are global, data-powered, and AI-enabled and may operate multiple other lines of profitable businesses. Should smaller studios downsize and sell content to the winners? Should they entice influencers and produce more content for social platforms? Or come together to form more competitive and capitalized alliances? At the minimum, studios will likely need to aggregate larger addressable audiences and secure much better ad tech.

The deeper challenge may be about mindsets. Traditional studios and streamers still seem organized around the same concepts and business models of TV and film that shaped entertainment for many decades. But costs and risk have narrowed cinema to very expensive and safe franchises, and if studios asked kids and teenagers what they think about the future of TV, they might answer, “What’s TV?”

Methodology

These insights are based on an online survey of 3,595 US consumers that was conducted in October 2024. Throughout this report, we reference generations. Our generational definitions are as follows: Generation Z (1997-2010), millennial (1983–1996), Generation X (1966–1982), boomers (1947-1965), and matures (1946 and prior). The survey was fielded by an independent research firm, and all data is weighted back to the most recent Census to give a representative view of US consumers.

Let’s make this work.

To view this social feed and similar content update your cookie settings to accept advertising and targeting cookies.

Let’s make this work.

To view this social feed and similar content update your cookie settings to accept advertising and targeting cookies.

Continue the conversation

Jana Arbanas

Doug Van Dyke

China Widener

Kevin Westcott

Jeff Loucks

by

China Widener

Jana Arbanas

Doug Van Dyke

Chris Arkenberg

Bree Matheson

Brooke Auxier

The authors would like to thank Akash Rawat, for his significant contributions to the data analysis, insights development, and writing for this report, along with Gautham Dutt for his design and visualization support. Many thanks also go to Andy Bayiates and Molly Piersol for their editorial and design contributions. The authors also extend appreciation to Danny Ledger, JD Tengberg, Stacy Hodgins, Leah Richardson, Chris Hirahatake, Noor Chawla, Rohith Nandagiri, Wenny Katzenstein, and Marc Weiner for their contributions to the co-creation and review of the questionnaire. Lastly, they would like to give sincere thanks to Kevin Downs, Amy Booth, and Alison Zink for their support and guidance throughout the process.

Cover image by: Alexis Werbeck

Visit the Deloitte Center for Technology, Media & Telecommunications

Access more insights for the technology, media, and entertainment; semiconductor; telecommunication; and sports sectors.